Estimated reading time: 17 minutes

Problems when hiring freelancers from abroad

This article deals with more than just the awarding of contracts to self-employed (freelance) business partners abroad. However, it was written with a direct focus on these issues.

More and more creative developers (programmers, website designers, copywriters, graphic designers, composers) have been leaving not only Germany, but often Europe as well for some time now. At the same time, however, fewer and fewer brilliant minds of this kind are growing up in Germany, Austria... perhaps even „slightly fewer“ in Switzerland. Why this is the case is an almost unnecessary consideration. As a managing director or senior executive, you yourself have probably long since recognized that the economic climate in the German-speaking regions of Europe is currently and will continue to adapt more to the development of the southern regions of Europe and the world instead of orienting itself towards the Nordic countries.

For you as a company/business, this means that you will increasingly have to potentially cover your need for skilled workers with employees from abroad. Which wouldn't be a problem „in itself“ if you could simply fall back on expatriate German-speaking experts abroad. There are no language problems, costs can be reduced for both sides, communication problems are practically non-existent thanks to fast Internet connections... although your potential freelancer / self-employed developer or designer probably has significantly faster and more reliable fiber optic lines abroad than you do in the industrial location of Germany. For example, I have 2 fiber optic lines from 2 different telecommunications providers in my house, plus a 5G wireless emergency modem ready for use at the window. In my former home near northern Hesse, our village of 450 souls had VDSL in the village, good for +/- 80 Mb... but all 120 local subscribers then went over the next mountain together via a 5 Ghz WLAN connection with a total capacity of 300 Mb. And when it started to rain, the connection was reliably lost after 10 seconds for 1 hour or longer anyway.

However, when you think about the topic of „employing skilled workers abroad“, a number of questions quickly arise:

- Invoicing: Are the invoices issued by the freelancer from abroad deductible as business expenses without limitation?

- Payment: Is the payment process seamlessly integrated into your financial accounting?

- Time difference: How do you communicate verbally and non-verbally with your partner abroad?

- Liability: What are the legal obligations regarding liability if the freelancer/partner is based abroad?

- Z4 Notification: Is your company subject to notification under the Foreign Trade and Payments Act (AWG)?

- Withholding tax: Do you have to withhold 15%-16% (including the immortal solidarity surcharge) from the freelancer invoice and report & pay it separately to your tax office?

This article addresses these core problems.

Invoicing

When your otherwise ingenious WordPress developer takes a photo of his hours from the cocktail napkin of a Thai beach bar in Pattaya and sends it to you via WhatsApp, it will certainly awaken a special kind of wanderlust in your accounting department.

However, this creative achievement will certainly not survive an audit or tax audit.

Similar requirements for invoices from abroad also apply - practically in all relevant national economies - for invoices from abroad (references e.g. here)

- Name and address of the company (providing the service)

- Your complete company address

- If possible, the (sales) tax identification number of the (service) provider

- Your own sales tax identification number

- Invoice date

- Ongoing Invoice number

- Description & number of products or services supplied

- The time of delivery or performance (general formulations such as „month of performance corresponds to month of invoice“ are permitted)

- Correct (!) final total - can be exciting with Word or Excel invoice forms

- The reference to the tax liability of the recipient of the service and invoice („In accordance with Section 13b UStG, reference is made to the tax liability of the recipient of the service. The tax rate is 19 percent.“)

By the way, a little fun fact: contrary to popular belief, your „consecutive invoice numbers“ must be no need be complete per se! However, they must be unique under all circumstances. If you enter your invoice numbers according to the pattern

year-month-day-customer-no. of the invoice to this customer on this day, then this is legal... but certainly not without gaps. However, if you create two invoices (or one invoice with a credit note) with the number 2022-06-08-08154711-01, this jeopardizes the input tax deduction and recognition as operating expenses by your customer. Then why not simply use a truly consecutive invoice number? Perhaps you or your partner don't want to make public how many bills you or your partner write each month...

I have been configuring, training & programming Navision Attain/Business Central & accounting/bookkeeping/archiving since 1993, also in international corporations. Please assume: All the above points are certainly included in my invoices.

Payment

Transfers to non-European countries can be very time-consuming. In addition, there is the risk that transfers to „critical“ countries can get „lost“ or that payments generate queries due to exchange rate fluctuations. Your partner should take this effort and risk on his own shoulders and not burden you with a payment by „cash deposit in Russian zloty to Western Union“.

Of course, I also follow this recommendation myself and maintain a European bank account with IBAN bank details and euros as the base currency. Would you like to transfer to a British, Australian or US account in the respective national currency? Talk to me, no problem. I have been training bookkeeping in Navision Attain/Business Central since 1993 and know various reasons why this can be advantageous or simply easier for you. In a personal meeting I can explain further advantages & possibilities of cooperation across national borders. Perhaps I can even save you the trouble of setting up a foreign limited company?

Address of your foreign partner

This was already an issue when it came to invoicing: the full address of your service provider. So far, so good. But here it can lead to Difficulties with announcement come! If your partner/service provider is in a ostracized country of the Eu, invoices from this location / service provider are generally not deductible as business expenses!

As of summer 2023, these are e.g. the following countries:

American Samoa, Anguilla, Bahamas, British Virgin Islands, Costa Rica, Fiji, Guam, Marshall Islands, Palau, Panama, Russia, Samoa, Trinidad and Tobago, Turks and Caicos Islands, U.S. Virgin Islands, Vanuatu.

In 2025, this list will include these countries:

American Samoa, Anguilla, Fiji, Guam, Palau, Panama, Russia, Samoa, Trinidad and Tobago, U.S. Virgin Islands, Vanuatu.

These countries are therefore excluded from this rule for the time being: Bahamas, British Virgin Islands, Costa Rica, Marshall Islands, Turks and Caicos Islands.

Freelancers/self-employed people therefore often choose the (perfectly legal) registration of a US LLC or a Canadian LLP (under modified British law). Perpetual travelers also like to try to „save“ themselves under this protective umbrella. It is important for you as a company that no fixed, verifiable place of residence (no tax residency) as well as a residence in one of the countries outlawed by the EU of your foreign partner will certainly result in at least queries during a company or business audit... with the risk that you may have to pay withholding tax, VAT or that the invoice(s) will be completely removed from your business expenses.

My registered and proven permanent residence is in the Philippines and I am also resident here for tax purposes. Germany also has a DTA (double taxation agreement) with the Philippines, which makes you even more secure. However, as a foreigner in the Philippines, I cannot easily obtain a tax number. This is also the case for other freelancers in other countries. Often the local company is then simply registered in the name of the mostly domestic partner, which can then lead to other problems for you as a European or German/Swiss/Austrian client/partner.

Therefore, for your and my security, despite the costs involved, I maintain a registered (incorporated) LLC in Kannada, and can therefore provide you with a legal, official, recognized tax number on my invoices. A tax number is not a 100% mandatory information on the invoices, but saves unnecessary queries during an audit or tax audit.

Time difference & communication

Opportunity and problem in one... This depends on mutual understanding... and on the extent of the time difference. In my case, for example, the time difference in summer is 6 hours, which has proved to be quite practical over time. I spend most of my time working in the morning, i.e. I don't disturb the employees during their daily work („Another user has changed the definition of the sales line table.“). And my afternoon then fits in perfectly with the office start time of 8 a.m. in Germany, e.g. for meetings or other adjustments. Time shifts beyond that could have a negative impact on collaboration... but they don't have to! Just give it a try.

Liability

Liability is an issue with Navision Financials/Business Central anyway. Who was really responsible for a certain misconduct? The user, because he simply expected something different from what Microsoft had defined? Microsoft, because MS installed a bug? The developer in your company? The former Navision partner? The current Navision / Business Central partner? Your freelancer? For this reason, any work I do for you is subject to a charge. It is completely irrelevant whether we are dealing with planning, implementation, major customization or whatever. However, this model may not be suitable for every job with a freelancer, e.g. if you commission a copyright-free jingle for your telephone system and this then turns out to be a plagiarism of a current pop song. In this case, however, I cannot make any recommendation at all. Because in such a case, you are liable in Germany even if your composer is based in Germany. Fortunately, I can rule this out for my programming work, as third-party developments generally do not meet my quality standards - and I do not compose jingles or design logos.

When does the reporting obligation for the Z4 notification apply?

Please note that larger invoices from e.g. me or more precise payments to me (over 12,500 euros New since 2025: 50,000 euros) automatically imposes an obligation to Notification according to AWG (Foreign Trade and Payments Act) §11 and §67 to the German Bundesbank. This applies not only to me, but to every money movement with foreign countries (even in the EU!) on your bank accounts. If you have already conducted transactions with foreign countries involving larger amounts, you are already subject to this reporting obligation under the Foreign Trade and Payments Act and must report to the Bundesbank every month by the 7th of the following month. If you do not make any sales abroad, you must still submit a false report, i.e. state that you did not make any sales abroad in the previous month. no longer have made sales abroad. Please also bear in mind that this concerns all sales from or to the Federal Republic of Germany, i.e. also to the EU! It is therefore more likely that your financial accounting department is already familiar with this anyway. Please also note the following: It is about the bank transaction, i.e. the transfer with the respective transfer amount. If you pay a higher invoice from or to a foreign country in 2 partial invoices of 10,000 euros each, or if you receive an invoice to a foreign country in two partial amounts, each of which is to be paid in one installment. under 12,500 euros New since 2025: Below 50,000 euros! the division of the Invoice and payment in e.g. 2 partial invoices/payment (be sure to clarify this with your accountant/auditor/tax consultant!) outside this regulation. These individual amounts no need should therefore be OK. However, this is usually a waste of time and effort: at some point, even if by mistake, an amount of money moves over this limit anyway, and - bang! - you are in the Z4 reporting obligation to the German Bundesbank, and from that point on you will never get out again. By the way: §11 also applies to any other financial transaction, e.g. also to a cross-border cash movement or the exchange of a gold Rolex from Germany for a Ford Mustang from France.

How can you generate these Z4 messages?

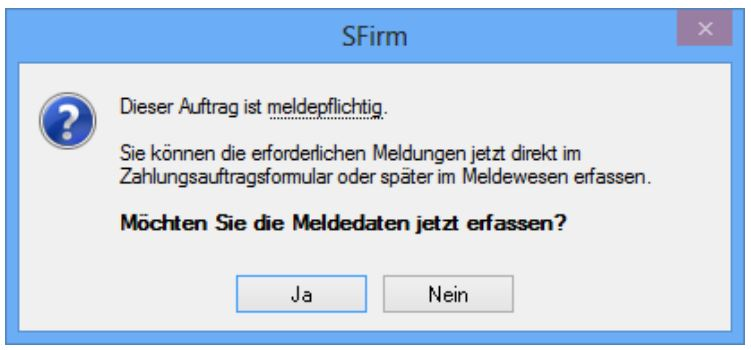

And what if you carry out regular bank transactions (bank transfers or cash receipts) with amounts over 50,000 euros? Depending on your Navision / Business Central setup, you may already have this included with your bank statement (e.g. if you use your own bank account for international transfers) or in your payment transactions (e.g. OP+ or Aquinet). Z4, Z5 (Z8, Z10) is not included in the standard system (and to my knowledge not in Aquinet & OPplus either) and must be created individually for you. Please contact me if required! Perhaps your bank/banking software creates this message for you instead of your Navision / Business Central, e.g. Sfirm from the German savings banks.

In the Z4 report, for example, the form of payment itself and the business transaction on which the payment is based must also be specified in the form of the associated Intrastat number.

Does this reporting obligation „Z4“ (Z5, Z10) also apply to private individuals?

You can find a very compact and easy to watch video here on this insanity of German legislation. Why insanity? Because the real money transfers simply take place despite this reporting obligation and are then simply labeled accordingly... or are then simply processed in the classic way using cash.

The reporting obligation for transfers abroad or from abroad to Germany according to Z4 essentially also applies to private individuals with private financial transactions, e.g. if you buy a house in Mallorca, a car in France or a plot of land in the Philippines/Thailand! The situation is a little more relaxed here and there is no monthly obligation to make a false declaration... but you must report as soon as the limit amount is exceeded. However, you can easily report this by telephone, for example. You can find more information on this in the video linked above, e.g. how to register with the Bundesbank for the simplified reporting of transfers to or from abroad, even without electronic reporting, e.g. using the Z4 or Z5 procedure with Navision / Business Central.

Withholding tax in accordance with Section 50a (1) No. 3 EStG for copyright-related services

And while we're at it: What about withholding tax if you do creative work, e.g. composing music, creating company logos, or... Programming work abroad? E.g. from me?

Essentially, you must deduct 15-16 % withholding tax from the invoice for all services from abroad affected by copyright law and pay this to the German tax office in Germany.

From my bills too? Loosely based on Radio Yerevan: In principle... No!

Basis for the obligation to pay withholding tax in accordance with Section 50a (1) no. 3 EStG

The facts of the case are quite complex, so please consult your tax advisor. I cannot provide tax advice.

You can find a very well-made video with lots of details here.

Here is another one.

Very briefly summarized: My services for you generally fall partly, since 2021 also in the sense of the law on withholding tax obviously no need into this Obligation to withhold and report withholding tax separately!

Which activities in the programming environment are not subject to the obligation to pay withholding tax?

Many of the services I provide for you have nothing to do with copyright anyway. Customize the invoice forms already predefined by Navision / Business Central? Create an explanation of the commission statement? A meeting to adjust the average cost price calculation? None of this is even covered by copyright law, as these activities lack the necessary level of creativity. This does affect my honor as a consultant and programmer, but there is a certain requirement for the „creativity“ of activities under copyright law, and this is the basis for withholding tax under Section 50a (1) No. 3 EStG. And due to the simple configurability (configuring is not programming) of Navision / Business Central, this is quite high.

Which programming activities affect copyright and therefore the obligation to pay withholding tax in accordance with Section 50a (1) no. 3 EStG?

What is the situation with complex programming tasks? Does § 50a para. 1 no. 3 EStG apply here?

My general terms and conditions, which you received at the beginning of our cooperation, already define that any programming I do on your behalf can be used by you for an unlimited period of time and space, and indirectly that you may make any adjustments to it and that the source code is also irrevocably transferred to you for this purpose in any case. To give you even more legal security, this is also noted on every invoice from me!

Why is a ban on the resale of the programs created relevant for (or against) the obligation to pay withholding tax in accordance with Section 50a (1) no. 3 EStG?

This does not mean that you can simply resell the complex programming work I have done in your Navision / Business Central. But, and this is the important detail: You do not acquire a license from me, but you acquire an unlimited and permanently usable solution including source code! This is also very important with regard to withholding tax! If you were allowed to resell the solutions I have created yourself, withholding tax would be due! Please also discuss this detail with your tax advisor.

You will find regular courses on what is possible with Idea and your ETRF data from Navision Financials Dynamics Attain or Microsoft Business Central BC365 here and here for further and more detailed information.

Please discuss this topic again with your tax advisor, as I have included so many sources in this article.

GDPR

What a bureaucracy from Germany... and actually only from Germany. But that doesn't help you, German courts don't judge with expertise and a sense of proportion when in doubt. In general, German courts do not have any significant expertise in IT issues, see Hamburg and Munich courts. You can find enough about Hamburg yourself if you google „copyright law“ and „Hamburg“, and I'll be happy to tell you about Munich over a beer here in Davao what my former employer Landefeld Druckluft und Hydraulik, Kassel, got up to in order to harm me and my customers... and how the Munich court dealt with it. Well, water under the bridge, all gone.

Back to the topic: Yes, I can also offer you a usable GDPR contract for external data processing - according to everything a specialist lawyer from Germany can say about it.